In the currently evident great American divide between rural and urban America, it must not be overlooked how deeply divided American Cities remain as well, at least economically. How drastic the opportunity divide is in Baltimore becomes clear by a just released report by the Washington based non-profit Corporation for Enterprise Development (CFED),

an "organization working at local, state and federal levels to create economic opportunity that alleviates poverty" that was founded in 1979.

|

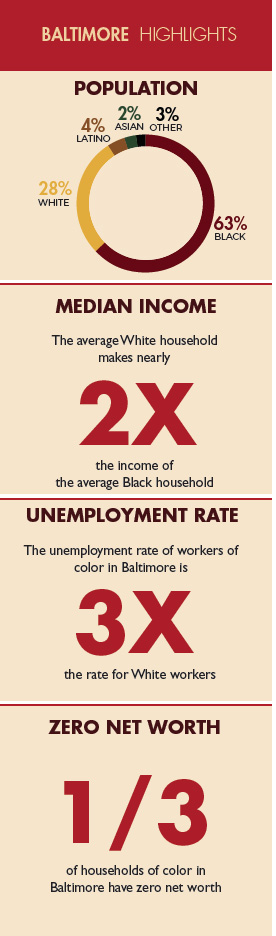

| CFED report |

The findings are startling: The mean black household income is just about half of what the mean white household income is. Two thirds of African American households have no cash reserves in an emergency (versus a still frightening one third for white households) and twice as many black households have zero net worth than whites.

Baltimore isn't even an extreme outlier in these measures but quite close to the national average.

|

| Baltimore's black poverty is close to the nation average. |

The national trend of revitalized cities attracts a lot of wealth to cities, be it through investments in development, industry relocation or wealthy residents. Clearly, some cities such as Boston, DC, San Francisco or Austin benefit much more from that trend than rustbelt cities like Baltimore, Detroit or Cleveland.

|

| The differences among cities: Austin and Detroit (Source: Prudential) |

Adam Smith immortalized "The Wealth of Nations," but prosperity in today’s world increasingly depends on the wealth of cities. In the United States, the 25 largest metropolitan areas churn out more than 40% of all economic output; the top 65% account for 65%. (Investors Daily, Feb 5, 2016)

|

| Education |

But the wealth bifurcation is evident even in flourishing cities because wealth is accumulating on a narrower and narrower base. An issue that cities cannot fix by themselves, no matter how many community benefit agreements or assessments.

Cities cannot redistribute wealth in a significant way nor can their initiatives in education, transportation, innovation or economic development compensate for the fact that so much money is made in the financial sector, through shares or through real estate, all fields mostly locked to the average citizen.

The top 10% of families -- those who had at least $942,000 -- held 76% of total wealth. The average amount of wealth in this group was $4 million.

Everyone else in the top 50% of the country accounted for 23% of total wealth, with an average of $316,000 per family.

That leaves just 1% of the total pie for the entire bottom half of the population.

|

| CFED Report |

The average held was $36,000 for families that fell in the 26th to 50th percentiles. But if they fell in the bottom quarter, they had zero wealth and in fact, were $13,000 in debt on average, CBO found. (CNN Money).

The concentration of wealth is half as accentuated in Europe and even less in Japan. That wealth distribution tracks race as closely as it does is prove how systemic racial discrimination in education, real estate, policing, business and many other fields has been over the decades locking blacks into poverty in harder to overcome ways than whites. That is not to say that there isn't white poverty, but it is much less accentuated in cities. Which gets us right back to the urban rural divide and why it is in large part also a racial one.

Klaus Philipsen, FAIA

The Racial Wealth Divide In Baltimore 2017

|

| household in come distribution shows the shape of the "white L" CFED Report |

|

| CFED Report |

|

| Median Household Income of blacks is just a bit more than that of whites (CFED Report) |

|

| Black households are twice as likely not to have a cash reserve for three months (CFED Report) |

|

Incarceration rates are far from the demographic base (62% versus 90%)

(CFED Report) |

No comments:

Post a Comment